266 THE AMERICAN ECONOMIC REVIEW bution of the return of any share,we shall assume for simplicity that they are at least in agreement as to the expected return.7 This way of characterizing uncertain streams merits brief comment. Notice first that the stream is a stream of profits,not dividends.As will become clear later,as long as management is presumed to be acting in the best interests of the stockholders,retained earnings can be regarded as equivalent to a fully subscribed,pre-emptive issue of common stock. Hence,for present purposes,the division of the stream between cash dividends and retained earnings in any period is a mere detail.Notice also that the uncertainty attaches to the mean value over time of the stream of profits and should not be confused with variability over time of the successive elements of the stream.That variability and uncer- tainty are two totally different concepts should be clear from the fact that the elements of a stream can be variable even though known with certainty.It can be shown,furthermore,that whether the elements of a stream are sure or uncertain,the effect of variability per se on the valua- tion of the stream is at best a second-order one which can safely be neg- lected for our purposes(and indeed most others too).8 The next assumption plays a strategic role in the rest of the analysis. We shall assume that firms can be divided into "equivalent return" classes such that the return on the shares issued by any firm in any given class is proportional to (and hence perfectly correlated with)the return on the shares issued by any other firm in the same class.This assumption implies that the various shares within the same class differ, at most,by a "scale factor."Accordingly,if we adjust for the difference in scale,by taking the ratio of the return to the expected return,the probability distribution of that ratio is identical for all shares in the class.It follows that all relevant properties of a share are uniquely char- acterized by specifying (1)the class to which it belongs and (2)its expected return. The significance of this assumption is that it permits us to classify firms into groups within which the shares of different firms are "homoge- neous,"that is,perfect substitutes for one another.We have,thus,an analogue to the familiar concept of the industry in which it is the com- modity produced by the firms that is taken as homogeneous.To com- plete this analogy with Marshallian price theory,we shall assume in the 7 To deal adequately with refinements such as differences among investors in estimates of expected returns would require extensive discussion of the theory of portfolio selection.Brief references to these and related topics will be made in the succeeding article on the general equilibrium model. 8 The reader may convince himself of this by asking how much he would be willing to rebate to his employer for the privilege of receiving his annual salary in equal monthly installments rather than in irregular amounts over the year.See also J.M.Keynes [10,esp.pp.53-541. This content downloaded from 202.120.21.61 on Thu,30 Nov 201707:07:36 UTC All use subject to http://about.jstor.org/terms

266 THE AMERICAN ECONOMIC REVIEW bution of the return of any share, we shall assume for simplicity that they are at least in agreement as to the expected return.7 This way of characterizing uncertain streams merits brief comment. Notice first that the stream is a stream of profits, not dividends. As will become clear later, as long as management is presumed to be acting in the best interests of the stockholders, retained earnings can be regarded as equivalent to a fully subscribed, pre-emptive issue of common stock. Hence, for present purposes, the division of the stream between cash dividends and retained earnings in any period is a mere detail. Notice also that the uncertainty attaches to the mean value over time of the stream of profits and should not be confused with variability over time of the successive elements of the stream. That variability and uncer- tainty are two totally different concepts should be clear from the fact that the elements of a stream can be variable even though known with certainty. It can be shown, furthermore, that whether the elements of a stream are sure or uncertain, the effect of variability per se on the valua- tion of the stream is at best a second-order one which can safely be neg- lected for our purposes (and indeed most others too).8 The next assumption plays a strategic role in the rest of the analysis. We shall assume that firms can be divided into "equivalent return" classes such that the return on the shares issued by any firm in any given class is proportional to (and hence perfectly correlated with) the return on the shares issued by any other firm in the same class. This assumption implies that the various shares within the same class differ, at most, by a "scale factor." Accordingly, if we adjust for the difference in scale, by taking the ratio of the return to the expected return, the probability distribution of that ratio is identical for all shares in the class. It follows that all relevant properties of a share are uniquely char- acterized by specifying (1) the class to which it belongs and (2) its expected return. The significance of this assumption is that it permits us to classify firms into groups within which the shares of different firms are "homoge- neous," that is, perfect substitutes for one another. We have, thus, an analogue to the familiar concept of the industry in which it is the com- modity produced by the firms that is taken as homogeneous. To com- plete this analogy with Marshallian price theory, we shall assume in the 7To deal adequately with refinements such as differences among investors in estimates of expected returns would require extensive discussion of the theory of portfolio selection. Brief references to these and related topics will be made in the succeeding article on the general equilibrium model. 8 The reader may convince himself of this by asking how much he would be willing to rebate to his employer for the privilege of receiving his annual salary in equal monthly installments rather than in irregular amounts over the year. See also J. M. Keynes [10, esp. pp. 53-541. This content downloaded from 202.120.21.61 on Thu, 30 Nov 2017 07:07:36 UTC All use subject to http://about.jstor.org/terms

MODIGLIANI AND MILLER:THEORY OF INVESTMENT 267 analysis to follow that the shares concerned are traded in perfect mar- kets under conditions of atomistic competition. From our definition of homogeneous classes of stock it follows that in equilibrium in a perfect capital market the price per dollar's worth of expected return must be the same for all shares of any given class.Or, equivalently,in any given class the price of every share must be propor- tional to its expected return.Let us denote this factor of proportionality for any class,say the kth class,by 1/p&.Then if denotes the price and is the expected return per share of the jth firm in class k,we must have: 1 (1) =一元; Pk or,equivalently, (2) =p&a constant for all firms j in class k. 帖 The constants pr(one for each of the k classes)can be given several economic interpretations:(a)From (2)we see that each pa is the ex- pected rate of return of any share in class k.(b)From (1)1/p&is the price which an investor has to pay for a dollar's worth of expected re- turn in the class k.(c)Again from(1),by analogy with the terminology for perpetual bonds,P can be regarded as the market rate of capitaliza- tion for the expected value of the uncertain streams of the kind gen- erated by the kth class of firms.10 B.Debt Financing and Its Efects on Security Prices Having developed an apparatus for dealing with uncertain streams we can now approach the heart of the cost-of-capital problem by drop- ping the assumption that firms cannot issue bonds.The introduction of debt-financing changes the market for shares in a very fundamental way.Because firms may have different proportions of debt in their capi- Just what our classes of stocks contain and how the different classes can be identified by outside observers are empirical questions to which we shall return later.For the present,it is sufficient to observe:(1)Our concept of a class,while not identical to that of the industry is at least closely related to it.Certainly the basic characteristics of the probability distributions of the returns on assets will depend to a significant extent on the product sold and the tech- nology used.(2)What are the appropriate class boundaries will depend on the particular prob- lem being studied.An economist concerned with general tendencies in the market,for example, might well be prepared to work with far wider classes than would be appropriate for an inves- tor planning his portfolio,or a firm planning its financial strategy. 10 We cannot,on the basis of the assumptions so far,make any statements about the rela- tionship or spread between the various p's or capitalization rates.Before we could do so we would have to make further specific assumptions about the way investors believe the proba- bility distributions vary from class to class,as well as assumptions about investors'preferences as between the characteristics of different distributions. This content downloaded from 202.120.21.61 on Thu,30 Nov 201707:07:36 UTC All use subject to http://about.jstor.org/terms

MODIGLIANI AND MILLER: THEORY OF INVESTMENT 267 analysis to follow that the shares concerned are traded in perfect mar- kets under conditions of atomistic competition.9 From our definition of homogeneous classes of stock it follows that in equilibrium in a perfect capital market the price per dollar's worth of expected return must be the same for all shares of any given class. Or, equivalently, in any given class the price of every share must be propor- tional to its expected return. Let us denote this factor of proportionality for any class, say the kth class, by l/Pk. Then if pi denotes the price and sj is the expected return per share of the jth firm in class k, we must have: (1) pj =-xj; Pk or, equivalently, (2) = Pk a constant for all firms j in class k. pi The constants Pk (one for each of the k classes) can be given several economic interpretations: (a) From (2) we see that each Pk iS the ex- pected rate of return of any share in class k. (b) From (1) l/Pk is the price which an investor has to pay for a dollar's worth of expected re- turn in the class k. (c) Again from (1), by analogy with the terminology for perpetual bonds, Pk can be regarded as the market rate of capitaliza- tion for the expected value of the uncertain streams of the kind gen- erated by the kth class of firms.10 B. Debt Financing and Its Effects on Security Prices Having developed an apparatus for dealing with uncertain streams we can now approach the heart of the cost-of-capital problem by drop- ping the assumption that firms cannot issue bonds. The introduction of debt-financing changes the market for shares in a very fundamental way. Because firms may have different proportions of debt in their capi- 9 Just what our classes of stocks contain and how the different classes can be identified by outside observers are empirical questions to which we shall return later. For the present, it is sufficient to observe: (1) Our concept of a class, while not identical to that of the industry is at least closely related to it. Certainly the basic characteristics of the probability distributions of the returns on assets will depend to a significant extent on the product sold and the tech- nology used. (2) What are the appropriate class boundaries will depend on the particular prob- lem being studied. An economist concerned with general tendencies in the market, for example, might well be prepared to work with far wider classes than would be appropriate for an inves- tor planning his portfolio, or a firm planning its financial strategy. 10 We cannot, on the basis of the assumptions so far, make any statements about the rela- tionship or spread between the various p's or capitalization rates. Before we could do so we would have to make further specific assumptions about the way investors believe the proba- bility distributions vary from class to class, as well as assumptions about investors' preferences as between the characteristics of different distributions. This content downloaded from 202.120.21.61 on Thu, 30 Nov 2017 07:07:36 UTC All use subject to http://about.jstor.org/terms

268 THE AMERICAN ECONOMIC REVIEW tal structure,shares of different companies,even in the same class,can give rise to different probability distributions of returns.In the language of finance,the shares will be subject to different degrees of financial risk or "leverage"and hence they will no longer be perfect substitutes for one another. To exhibit the mechanism determining the relative prices of shares under these conditions,we make the following two assumptions about the nature of bonds and the bond market,though they are actually stronger than is necessary and will be relaxed later:(1)All bonds(in- cluding any debts issued by households for the purpose of carrying shares)are assumed to yield a constant income per unit of time,and this income is regarded as certain by all traders regardless of the issuer. (2)Bonds,like stocks,are traded in a perfect market,where the term perfect is to be taken in its usual sense as implying that any two com- modities which are perfect substitutes for each other must sell,in equi- librium,at the same price.It follows from assumption(1)that all bonds are in fact perfect substitutes up to a scale factor.It follows from as- sumption(2)that they must all sell at the same price per dollar's worth of return,or what amounts to the same thing must yield the same rate of return.This rate of return will be denoted by r and referred to as the rate of interest or,equivalently,as the capitalization rate for sure streams.We now can derive the following two basic propositions with respect to the valuation of securities in companies with different capital structures: Proposition I.Consider any company j and let X;stand as before for the expected return on the assets owned by the company (that is,its expected profit before deduction of interest).Denote by D;the market value of the debts of the company;by S;the market value of its com- mon shares;and by V;=S;++D;the market value of all its securities or, as we shall say,the market value of the firm.Then,our Proposition I asserts that we must have in equilibrium: (3) Vi=(Sj+Di)=Xi/pe,for any firm j in class k. That is,the markel value of any firm is independen of its capital structure and is given by capitalizing its expected relurn at the rale p&appropriate to its class. This proposition can be stated in an equivalent way in terms of the firm's"average cost of capital,"Xi/Vi,which is the ratio of its expected return to the market value of all its securities.Our proposition then is: 又 X (4) -pa,for any firm j,in class k. (S;+D)V That is,the average cosl of capital to any firm is complelely independent of This content downloaded from 202.120.21.61 on Thu,30 Nov 201707:07:36 UTC All use subject to http://about jstor.org/terms

268 THE AMERICAN ECONOMIC REVIEW tal structure, shares of different companies, even in the same class, can give rise to different probability distributions of returns. In the language of finance, the shares will be subject to different degrees of filancial risk or "leverage" and hence they will no longer be perfect substitutes for one another. To exhibit the mechanism determining the relative prices of shares under these conditions, we make the following two assumptions about the nature of bonds and the bond market, though they are actually stronger than is necessary and will be relaxed later: (1) All bonds (in- cluding any debts issued by households for the purpose of carrying shares) are assumed to yield a constant income per unit of time, and this income is regarded as certain by all traders regardless of the issuer. (2) Bonds, like stocks, are traded in a perfect market, where the term perfect is to be taken in its usual sense as implying that any two com- modities which are perfect substitutes for each other must sell, in equi- librium, at the same price. It follows from assumption (1) that all bonds are in fact perfect substitutes up to a scale factor. It follows from as- sumption (2) that they must all sell at the same price per dollar's worth of return, or what amounts to the same thing must yield the same rate of return. This rate of return will be denoted by r and referred to as the rate of interest or, equivalently, as the capitalization rate for sure streams. We now can derive the following two basic propositions with respect to the valuation of securities in companies with different capital structures: Proposition I. Consider any company j and let Xi stand as before for the expected return on the assets owned by the company (that is, its expected profit before deduction of interest). Denote by Di the market value of the debts of the company; by Sj the market value of its com- mon shares; and by Vj=Sj+Dj the market value of all its securities or, as we shall say, the market value of the firm. Then, our Proposition I asserts that we must have in equilibrium: (3) Vi (Sj + Dj) = Xjl/pk, for any firm j in class k. That is, the market value of any firm is indepezdentt of its capital structure and is given by capitalizinzg its expected return at the rate Pk appropriate to its class. This proposition can be stated in an equivalent way in terms of the firm's "average cost of capital," Xj/Vj, which is the ratio of its expected return to the market value of all its securities. Our proposition then is: xj Xj (4) - = Pk, for any firm j, in class k. (Sj + Di) Va That is, thec average cost of capital, to any firm 'IS comipletely independent of This content downloaded from 202.120.21.61 on Thu, 30 Nov 2017 07:07:36 UTC All use subject to http://about.jstor.org/terms

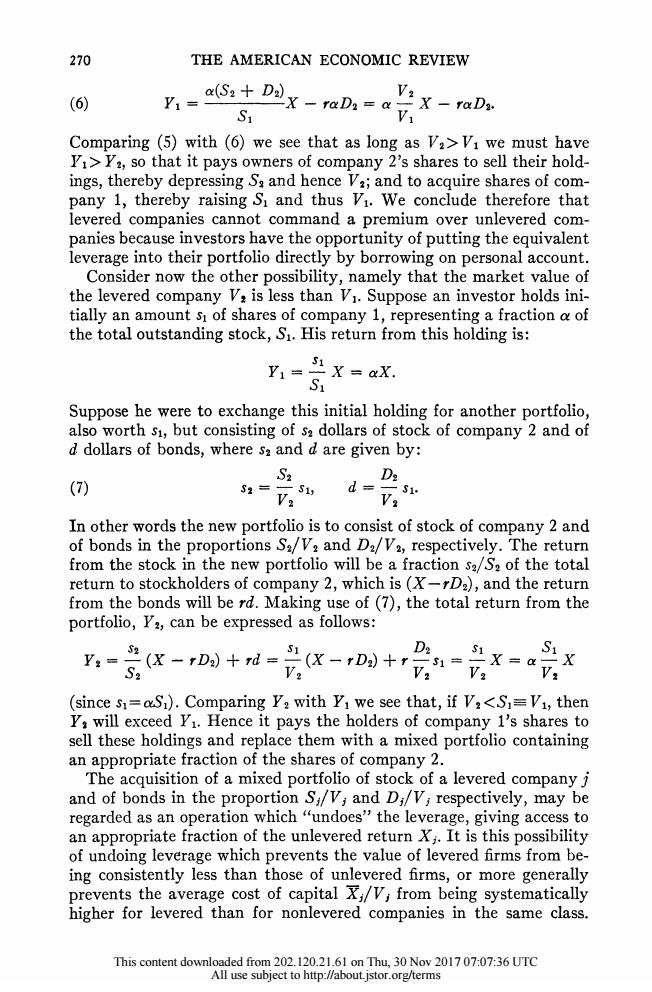

MODIGLIANI AND MILLER:THEORY OF INVESTMENT 269 its capital structure and is egual to the capitalization rate of a pure equity stream of its class. To establish Proposition I we will show that as long as the relations (3)or(4)do not hold between any pair of firms in a class,arbitrage will take place and restore the stated equalities.We use the term arbitrage advisedly.For if Proposition I did not hold,an investor could buy and sell stocks and bonds in such a way as to exchange one income stream for another stream,identical in all relevant respects but selling at a lower price.The exchange would therefore be advantageous to the inves- tor quite independently of his attitudes toward risk.As investors exploit these arbitrage opportunities,the value of the overpriced shares will fall and that of the underpriced shares will rise,thereby tending to eliminate the discrepancy between the market values of the firms. By way of proof,consider two firms in the same class and assume for simplicity only,that the expected return,X,is the same for both firms. Let company 1 be financed entirely with common stock while company 2 has some debt in its capital structure.Suppose first the value of the levered firm,V2,to be larger than that of the unlevered one,Vi.Con- sider an investor holding sa dollars'worth of the shares of company 2, representing a fraction a of the total outstanding stock,S2.The return from this portfolio,denoted by Y2,will be a fraction a of the income available for the stockholders of company 2,which is equal to the total return X2 less the interest charge,rDa.Since under our assumption of homogeneity,the anticipated total return of company 2,X2,is,under all circumstances,the same as the anticipated total return to company 1,Xi,we can hereafter replace X2 and Xi by a common symbol X. Hence,the return from the initial portfolio can be written as: (5) Y2=a(X-rD2). Now suppose the investor sold his aS:worth of company 2 shares and acquired instead an amount s=(S2+D)of the shares of company 1. He could do so by utilizing the amount aS2 realized from the sale of his initial holding and borrowing an additional amount aDa on his own credit,pledging his new holdings in company 1 as a collateral.He would thus secure for himself a fraction s1/S1=a(S2+D2)/S1 of the shares and earnings of company 1.Making proper allowance for the interest pay- ments on his personal debt aDa,the return from the new portfolio,Yi,is given by: u In the language of the theory of choice,the exchanges are movements from inefficient points in the interior to efficient points on the boundary of the investor's opportunity set;and not movements between efficient points along the boundary.Hence for this part of the analysis nothing is involved in the way of specific assumptions about investor attitudes or behavior other than that investors behave consistently and prefer more income to less income,ceferis paribus. This content downloaded from 202.120.21.61 on Thu,30 Nov 201707:07:36 UTC All use subject to http://about.jstor.org/terms

MODIGLIANI AND MILLER: THEORY OF INVESTMENT 269 its capital structure and is equal to the capitalization rate of a pure equity stream of its class. To establish Proposition I we will show that as long as the relations (3) or (4) do not hold between any pair of firms in a class, arbitrage will take place and restore the stated equalities. We use the term arbitrage advisedly. For if Proposition I did not hold, an investor could buy and sell stocks and bonds in such a way as to exchange one income stream for another stream, identical in all relevant respects but selling at a lower price. The exchange would therefore be advantageous to the inves- tor quite independently of his attitudes toward risk.1' As investors exploit these arbitrage opportunities, the value of the overpriced shares will fall and that of the underpriced shares will rise, thereby tending to eliminate the discrepancy between the market values of the firms. By way of proof, consider two firms in the same class and assume for simplicity only, that the expected return, X, is the same for both firms. Let company 1 be financed entirely with common stock while company 2 has some debt in its capital structure. Suppose first the value of the levered firm, V2, to be larger than that of the unlevered one, Vi. Con- sider an investor holding S2 dollars' worth of the shares of company 2, representing a fraction a of the total outstanding stock, S2. The return from this portfolio, denoted by Y2, will be a fraction ac of the income available for the stockholders of company 2, which is equal to the total return X2 less the interest charge, rD2. Since under our assumption of homogeneity, the anticipated total return of company 2, X2, is, under all circumstances, the same as the anticipated total return to company 1, XI, we can hereafter replace X2 and Xi by a common symbol X. Hence, the return from the initial portfolio can be written as: (5) Y2- a(X - rD2). Now suppose the investor sold his aS2 worth of company 2 shares and acquired instead an amount Sl= a(S2+D2) of the shares of company 1. He could do so by utilizing the amount aS2 realized from the sale of his initial holding and borrowing an additional amount aD2 on his own credit, pledging his new holdings in company 1 as a collateral. He would thus secure for himself a fraction sl/S = a(S2+?D2)/S, of the shares and earnings of company 1. Making proper allowance for the interest pay- ments on his personal debt aD2, the return from the new portfolio, Y1, is given by: 11 In the language of the theory of choice, the exchanges are movements from inefficient points in the interior to efficient points on the boundary of the investor's opportunity set; and not movements between efficient points along the boundary. Hence for this part of the analysis nothing is involved in the way of specific assumptions about investor attitudes or behavior other than that investors behave consistently and prefer more income to less income, ceteris paribus. This content downloaded from 202.120.21.61 on Thu, 30 Nov 2017 07:07:36 UTC All use subject to http://about.jstor.org/terms

270 THE AMERICAN ECONOMIC REVIEW (6) a(Sa+D2x raDa ay:X-raDy. Y1= S1 Comparing (5)with (6)we see that as long as Va>Vi we must have Yi>Ya,so that it pays owners of company 2's shares to sell their hold- ings,thereby depressing Sa and hence Va;and to acquire shares of com- pany 1,thereby raising S and thus Vi.We conclude therefore that levered companies cannot command a premium over unlevered com- panies because investors have the opportunity of putting the equivalent leverage into their portfolio directly by borrowing on personal account. Consider now the other possibility,namely that the market value of the levered company V:is less than Vi.Suppose an investor holds ini- tially an amount s of shares of company 1,representing a fraction a of the total outstanding stock,S1.His return from this holding is: 1=X=ax. Suppose he were to exchange this initial holding for another portfolio, also worth si,but consisting of sa dollars of stock of company 2 and of d dollars of bonds,where sa and d are given by: g D2 (7) S2= S1,d=s1. V2 V2 In other words the new portfolio is to consist of stock of company 2 and of bonds in the proportions S2/V2 and D2/V2,respectively.The return from the stock in the new portfolio will be a fraction sa/Se of the total return to stockholders of company 2,which is(X-rDa),and the return from the bonds will be rd.Making use of (7),the total return from the portfolio,Y2,can be expressed as follows: -K-则+d-元X-0+,= D2 S1 S1 -X a V2 (since s1=aS1).Comparing Y2 with Yi we see that,if V2<S=Vi,then Ya will exceed Y1.Hence it pays the holders of company 1's shares to sell these holdings and replace them with a mixed portfolio containing an appropriate fraction of the shares of company 2. The acquisition of a mixed portfolio of stock of a levered company j and of bonds in the proportion Si/V;and D;/V;respectively,may be regarded as an operation which"undoes"the leverage,giving access to an appropriate fraction of the unlevered return Xi.It is this possibility of undoing leverage which prevents the value of levered firms from be- ing consistently less than those of unlevered firms,or more generally prevents the average cost of capital Xi/V;from being systematically higher for levered than for nonlevered companies in the same class. This content downloaded from 202.120.21.61 on Thu,30 Nov 201707:07:36 UTC All use subject to http://about.jstor.org/terms

270 THE AMERICAN ECONOMIC REVIEW (6) - cx~(S2 + D2) V2 (6) Y, = t(S2 X - raD2 = a - X - raD2. Si V1 Comparing (5) with (6) we see that as long as V2> V1 we must have Y1 > Y2, so that it pays owners of company 2's shares to sell their hold- ings, thereby depressing S2 and hence V2; and to acquire shares of com- pany 1, thereby raising Si and thus V1. We conclude therefore that levered companies cannot command a premium over unlevered com- panies because investors have the opportunity of putting the equivalent leverage into their portfolio directly by borrowing on personal account. Consider now the other possibility, namely that the market value of the levered company V2 is less than V1. Suppose an investor holds ini- tially an amount s1 of shares of company 1, representing a fraction cx of the total outstanding stock, Si. His return from this holding is- Si Y -S X = agx. Si Suppose he were to exchange this initial holding for another portfolio, also worth s1, but consisting of S2 dollars of stock of company 2 and of d dollars of bonds, where s2 and d are given by: S2 D2 (7) S2=- 1, d =-s. V2 V2 In other words the new portfolio is to consist of stock of company 2 and of bonds in the proportions S2/V2 and D2/V2, respectively. The return from the stock in the new portfolio will be a fraction S2/S2 of the total return to stockholders of company 2, which is (X- rD2), and the return from the bonds will be rd. Making use of (7), the total return from the portfolio, Y2, can be expressed as follows: S2 D2 s1 S Y2= - (X - rD2) + rd = - (X - rD2) + r V-S =- X = - X S2 V2 V2 V2 V2 (since si = aSi). Comparing Y2 with Yi we see that, if V2 <SI V1, then Y2 will exceed Y1. Hence it pays the holders of company l's shares to sell these holdings and replace them with a mixed portfolio containing an appropriate fraction of the shares of company 2. The acquisition of a mixed portfolio of stock of a levered company j and of bonds in the proportion Sj/Vj and D1/Vj respectively, may be regarded as an operation which "undoes" the leverage, giving access to an appropriate fraction of the unlevered return Xj. It is this possibility of undoing leverage which prevents the value of levered firms from be- ing consistently less than those of unlevered firms, or more generally prevents the average cost of capital jl/Vj from being systematically higher for levered than for nonlevered companies in the same class. This content downloaded from 202.120.21.61 on Thu, 30 Nov 2017 07:07:36 UTC All use subject to http://about.jstor.org/terms