CHAPTER 11 MORAL HAZARD

CHAPTER 11 MORAL HAZARD

WHAT IS MORAL HAZARD? Ch 11 Moral Hazard

Ch 11 | Moral Hazard WHAT IS MORAL HAZARD?

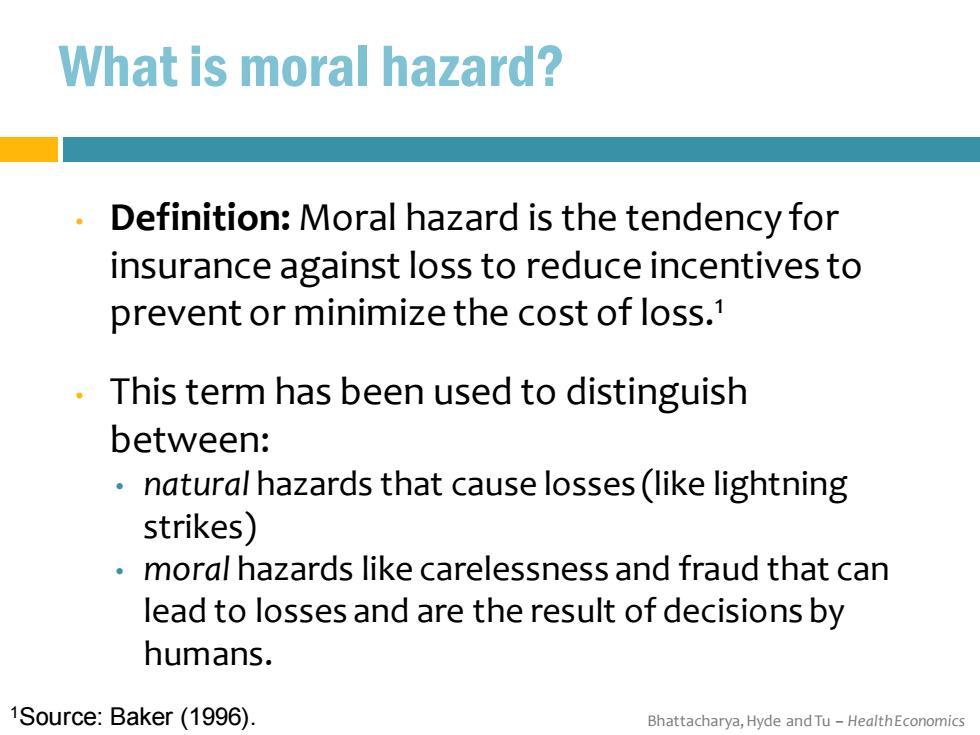

What is moral hazard? 。 Definition:Moral hazard is the tendency for insurance against loss to reduce incentives to prevent or minimize the cost of loss.1 This term has been used to distinguish between: natural hazards that cause losses(like lightning strikes) moral hazards like carelessness and fraud that can lead to losses and are the result of decisions by humans. 1Source:Baker(1996). Bhattacharya,Hyde and Tu-HealthEconomics

Bhattacharya, Hyde and Tu – Health Economics What is moral hazard? • Definition: Moral hazard is the tendency for insurance against loss to reduce incentives to prevent or minimize the cost of loss.1 • This term has been used to distinguish between: • natural hazards that cause losses (like lightning strikes) • moral hazards like carelessness and fraud that can lead to losses and are the result of decisions by humans. 1Source: Baker (1996)

Moral hazard with health insurance Insured people take risks with their health that similar uninsured people would not take,and demand more expensive treatment from their doctors when they get sick. Moral hazard is the downside of health insurance because it raises society's level of health care expenditures. Bhattacharya,Hyde and Tu-HealthEconomics

Bhattacharya, Hyde and Tu – Health Economics Moral hazard with health insurance • Insured people take risks with their health that similar uninsured people would not take, and demand more expensive treatment from their doctors when they get sick. • Moral hazard is the downside of health insurance because it raises society’s level of health care expenditures

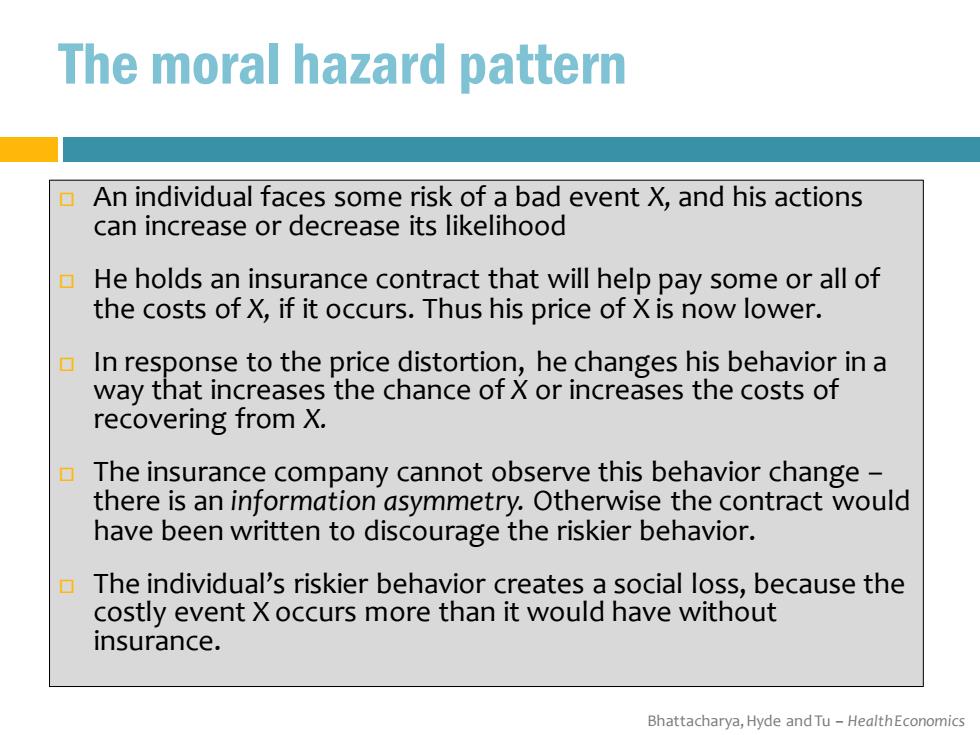

The moral hazard pattern An individual faces some risk of a bad event X,and his actions can increase or decrease its likelihood He holds an insurance contract that will help pay some or all of the costs of X,if it occurs.Thus his price of X is now lower. In response to the price distortion,he changes his behavior in a way that increases the chance of X or increases the costs of recovering from X. The insurance company cannot observe this behavior change- there is an information asymmetry.Otherwise the contract would have been written to discourage the riskier behavior. The individual's riskier behavior creates a social loss,because the costly event X occurs more than it would have without insurance. Bhattacharya,Hyde and Tu-HealthEconomics

Bhattacharya, Hyde and Tu – Health Economics The moral hazard pattern An individual faces some risk of a bad event X, and his actions can increase or decrease its likelihood He holds an insurance contract that will help pay some or all of the costs of X, if it occurs. Thus his price of X is now lower. In response to the price distortion, he changes his behavior in a way that increases the chance of X or increases the costs of recovering from X. The insurance company cannot observe this behavior change – there is an information asymmetry. Otherwise the contract would have been written to discourage the riskier behavior. The individual’s riskier behavior creates a social loss, because the costly event X occurs more than it would have without insurance